Electra Battery Materials valued well below asset value

Electra Battery Materials has a cobalt sulfate refinery coming online in Quebec in about 15-16 months that will be the only on in N. America! Worth far more than the market cap...

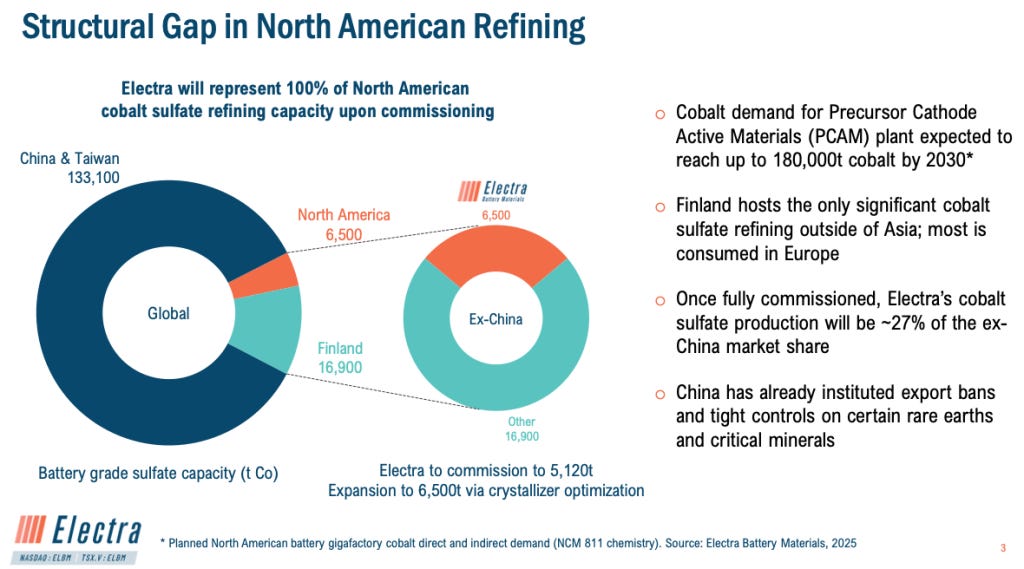

Electra Battery Materials (TSX-v: ELBM) / (NASDAQ: ELBM) is 100% owner of a valuable refining complex in NE Ontario, a facility that will produce 100% of N. America’s cobalt (“Co”) sulfate (up to 6,500 tonnes/yr.). Production is expected to start in 2H/27.

Demand for Lithium-ion batteries is coming in stronger than expected due in large part to stationary Battery Energy Storage Systems (“BESS”) adoption.

The IEA projects Co demand will rise from 213,000 tonnes in 2023 to 344,00 by 2030, and 454,000 by 2040. According to various sources, the Co sulphate market specifically is forecast to have a roughly a 5-6% CAGR through 2032–2035.

Electra’s Battery Materials Complex (“BMC“) has a third-party (Hatch) estimated replacement cost of US$250M, (in my view, possibly > US$300M, the assessment is a few years old, and inflationary pressures have been significant).

Importantly, it would likely take over five years to plan, fund, PERMIT, build, and commission a new facility like Electra’s. Compare that US$250M+ to Electra’s enterprise value {market cap + debt – cash} of ~US$113M (US$0.60/shr.).

Moreover, in plenty of places around the world, permits might never be approved. I think there should be a discernible floor forming, above today’s level, as we get approach commissioning.

Understandably, all eyes are on the Middle East, but a critically important second-order ramification is deteriorating relations between China & the West.

China has come out against the U.S./Israel’s war on Iran. In mid-April 2026, Trump threatened to impose a new 50% tariff on China upon reports that Beijing might deliver air defense systems to Iran.

And, the U.S. clearly doesn’t want China to buy Iranian oil — a directive that China has rejected.

What do heightened geopolitical events have to do with Electra Battery Materials? As the bifurcation between East & West only grows, having strategic assets in safe, prolific jurisdictions like Canada & the U.S. is increasingly important.

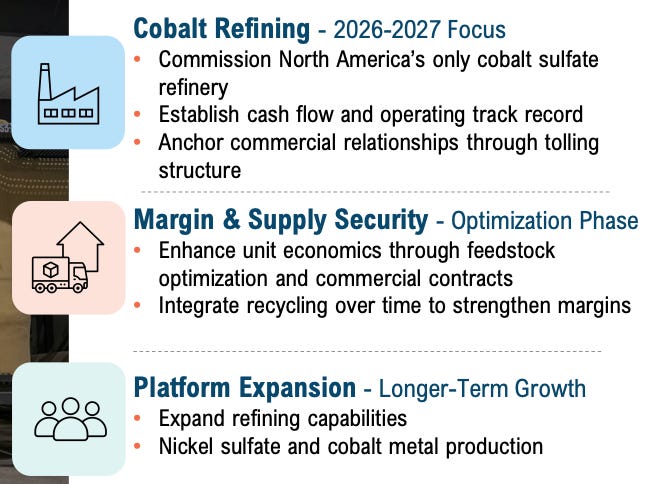

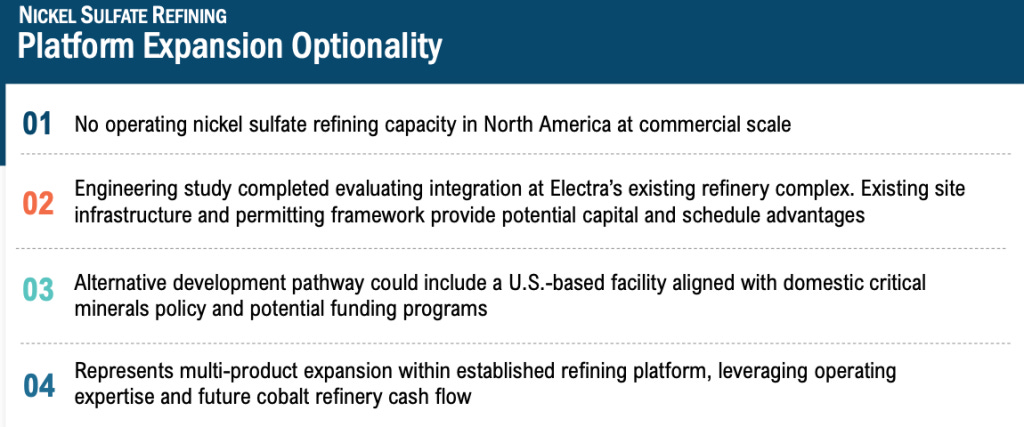

Electra’s BMC is on a sizable industrial site that could (subject to more studies & investment capital) host other operations, most notably black mass recycling and nickel sulfate production. That is likely 2H/27 or 2028 business, for now the main focus is Co sulfate.

In my opinion, the optionality of being able to expand into new cash flowing segments has tangible value. These segments, if deemed attractive and viable, are not 6-8 years away, just 2 or 3.

Moreover, there’s clear evidence that Canada is looking to diversify away the U.S., as it should. On May 4th, the Company announced a C$20M funding package for Electra’s ongoing enhancement of the refinery complex.

While the mix of free-money grant vs. debt is not specified in the PR, my understanding is that ~20-25% of the $20M is a grant. Importantly, the debt component of is VERY low cost, a rumored interest rate below 4%, and a reported maturity of 22 years!

As per the press release, this is not new funding, but a binding commitment of a prior LOI. Taken together with LG Energy Solution’s March, 2026 commitment to extend its off-take agreement to six years, there’s considerable de-risking going on here.

CEO Trent Mell is in Washington D.C. this week. He could be talking about Electra’s Idaho assets, Ontario’s BMC and/or other initiatives. He and/or members of the Electra team visit D.C. several times a year.

Hard assets like mills and processing facilities can produce cash flow for many decades. Strategic assets like Electra’s BMC, are worth more today than a year or two ago. Owning 100% of the BMC provides considerable financial optionality.

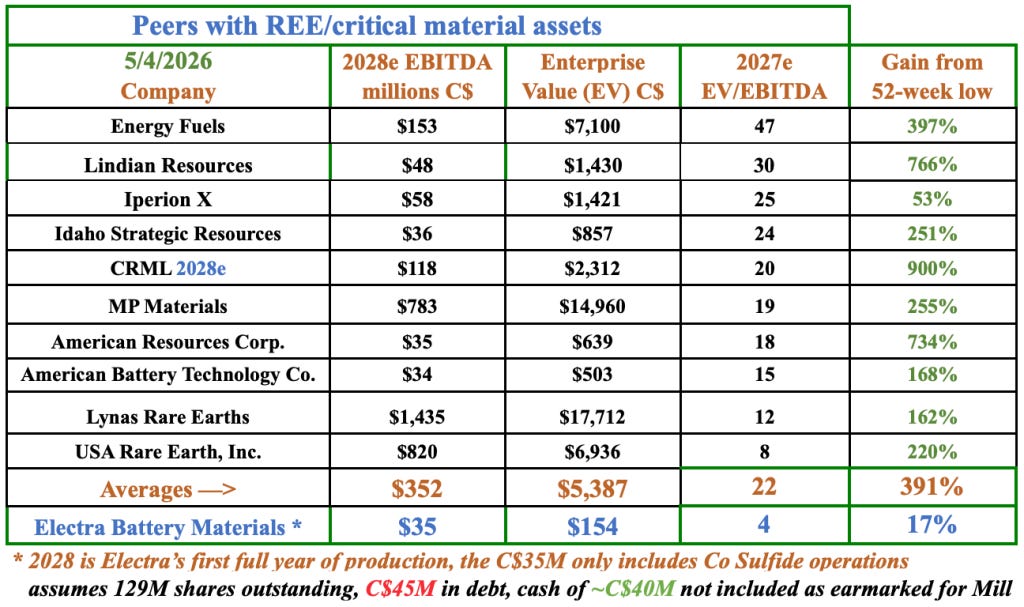

5 peers have under C$60M in 2028e EBITDA...

Today’s Company valuation is roughly a third of replacement cost, and one gets Electra’s U.S. assets for free.

Cash on hand of ~C$40M is assumed to be fully utilized by the BMC refurbishment activities & further de-risking in the U.S. (more on U.S. assets later). NOTE, there’s a slug of warrants with a strike price of ~C$1.70 that would bring in nearly C$80M.

Importantly, the BMC is permitted & fully-funded. Technical risk of the expansion is relatively low. Unlike juniors developing mines with 10-20 year lives, Electra’s BMC could be operating into the next century, reinventing itself along the way as needed.

By establishing N. America’s only Co sulfate refinery, sourcing diversified feedstock, and advancing recycling operations, (but probably not before 2H/27 on recycling), Electra’s building a platform that’s resilient across cycles.

Electra’s BMC, a substantial, 50+ year hard asset

As a reminder, Electra’s BMC has done test runs of black mass to recycle end-of-life Li-ion batteries to recover Li, Co & Ni.

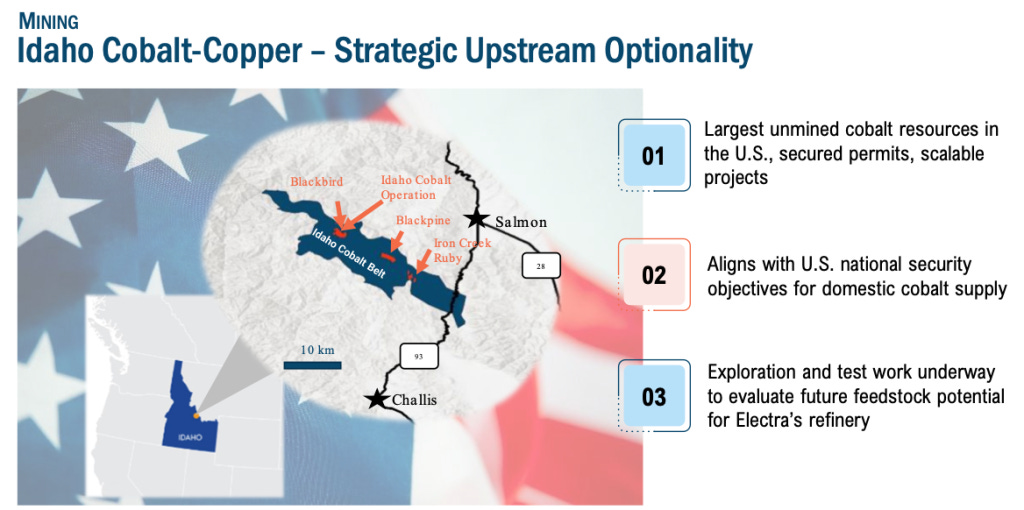

Electra also has a strategic Co & copper project in the U.S. state of Idaho. The resource size is not large, but there’s ample room to grow it with more drilling. As it stands, it’s already one of the larger Co deposits in the U.S.

Analysts described 2025 as “particularly troubled” for mined copper supply, with cumulative hits (e.g., Grasberg, El Teniente, Kamoa-Kakula) reducing output by up to 5-6% — far exceeding typical annual disruption allowances (typically 2-4%).

Cu & Co are critical materials in the U.S. What better place than mining-friendly Idaho (top quartile of latest annual Fraser Institute Mining Survey) for the U.S. to lock down long-term sustainable supply?

Electra has three opportunities that don’t get discussed much, but could rise in importance (and value) over time. Readers might have noticed that nickel is near a 2-yr high, ~US$19,500/tonne. Electra has a nickel sulfate refining scoping study under its belt.

Management has an option to help build/co-locate a second Co sulfate refinery with precursor makers in Quebec (a Li-ion battery hub in Becancour). Finally, as mentioned, the recycling of black mass (shredded end of life Li-ion batteries) to recover lithium, nickel & Co.

What ties these opportunities together is strong Co & lithium prices, (lithium has tripled from last Summer’s lows), a meaningfully recovery in nickel, and redoubled efforts to on-shore critical supply chains in N. America.

Readers should note that Electra Battery Materials (TSX-v: ELBM) / (NASDAQ: ELBM) has been very volatile and will likely continue to be.

However, as a hard asset company with cash flow beginning next year, and being fully-funded [before working capital needs] to finish retrofitting/enhancing its highly strategic & flexible BMC, it’s possibly a good time for a closer look at this investment opportunity.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER] ) about Electra Battery Materials, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Electra Battery Materials are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Electra Battery Materials was an advertiser on [ER] and Peter Epstein owned shares in the company.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector, or investment topic.